Bank Overdraft Fees: How They Work and How to Avoid Them

When it comes to managing personal finances, few things can create as much stress and frustration as overdraft fees. These fees occur when you spend more money than you have available in your bank account, leading to a negative balance and potentially expensive charges from your bank. This article will explore how bank overdraft fees work and provide some helpful tips on how to avoid them.

Understanding Overdraft Fees

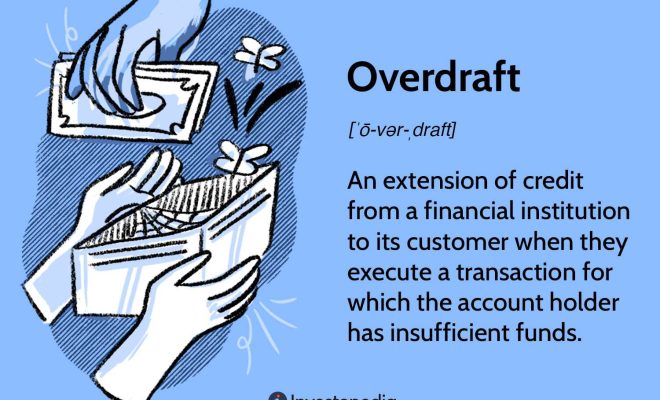

Overdraft fees are imposed by banks when a customer withdraws more money than they have available in their checking account or overdraws using a check, debit card, automatic bill payment, or other transaction types. When this happens, the bank covers the shortfall by extending a line of credit to the account holder. In return for this service, the bank charges an overdraft fee, which typically ranges from $25 to $35 per occurrence.

Different Types of Overdraft Protection

To help customers avoid overdraft fees, many banks offer overdraft protection services. There are several types of protection available:

1. Linking a Savings Account: By linking your savings account to your checking account, you can automatically transfer funds between them if you overdraw your checking balance.

2. Line of Credit: Some banks offer an overdraft line of credit that functions similarly to a credit card. If you overdraw your account, the bank will transfer funds from your line of credit to cover the transaction.

3. Overdraft Protection Plans: These plans typically involve a monthly fee and grant you a specific amount of leeway in case of an overdraft. Instead of charging a standard overdraft fee for each occurrence, these plans charge lower fees based on usage.

Tips for Avoiding Overdraft Fees

There are several strategies for avoiding overdraft fees:

1. Track Your Expenses: Regularly monitor your account balance and transactions by using mobile banking apps or online banking services.

2. Set Up Account Alerts: Many banks allow customers to set up email or text alerts when a balance reaches a certain threshold, helping you stay informed about your account status.

3. Create a Budget: Establishing a budget can help you avoid overdraft fees by encouraging more responsible spending habits and ensuring that you maintain a sufficient account balance.

4. Opt-Out of Overdraft Coverage: By law, banks cannot automatically enroll customers in overdraft coverage for ATM and one-time debit card transactions. You can choose to opt-out of this protection, resulting in declined transactions instead of costly overdraft fees. Be cautious, though, as bounced checks and recurring bill payments may still trigger overdraft charges.

5. Maintain an Emergency Fund: Having a dedicated savings account for emergencies can provide a buffer if you risk overdrawing your checking account.

In conclusion, understanding how bank overdraft fees work and implementing effective strategies to avoid them can save you a significant amount of money in the long run. By carefully monitoring your expenses, setting up alerts, and utilizing available resources such as overdraft protection plans, you can steer clear of these costly fees and maintain better financial health